{kind=link}

Introduction

As we approach the end of 2020, Mike and I thought it would be interesting to take a look at the overall state of the camera industry through two lenses: production and usage.

By triangulating multiple data sources (see a full list of sources at the bottom of the post) we wanted to see the stories and trends the data would reveal about what lies ahead for the industry as a whole and for individual manufacturers based on how photographers, amateur and professional alike, use their products.

We look at both dedicated camera manufacturers as well as the leading smartphone makers. The growth of smartphones as devices for casual and dedicated photography has been the dominant industry story of the past decade.

This post starts with an industry overview using CIPA data for cameras and Counterpoint and Facebook data for mobile. It then presents snapshots of every major individual camera and smartphone manufacturer. The conclusion summarises the trends and looks ahead.

Industry Overview

Production & Sales

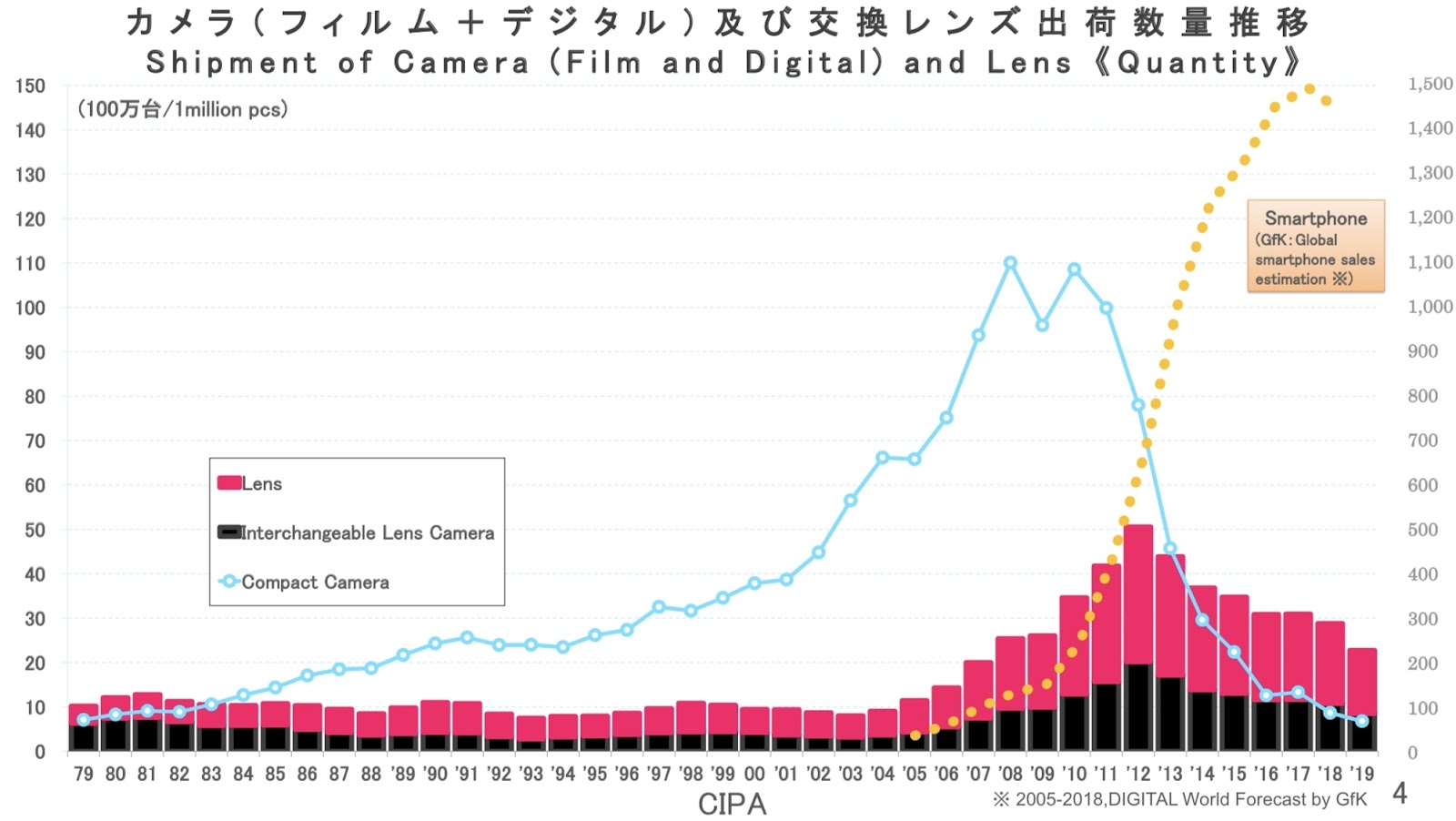

We’ve all seen this chart of some version of it:

The story it tells is a familiar one: starting in 2011, the mass adoption of smartphones correlates perfectly with the decline of compact camera sales and, since 2013, the continued growth of smartphones appears to have exerted similar downward pressure on the sales of interchangeable lens cameras. The sales of lenses (pink bar) however have proven to be somewhat more resilient; we discuss some reasons why below, and we have yet to see what the plateau in smartphone sales (as adoption approaches saturation) means for the camera industry.

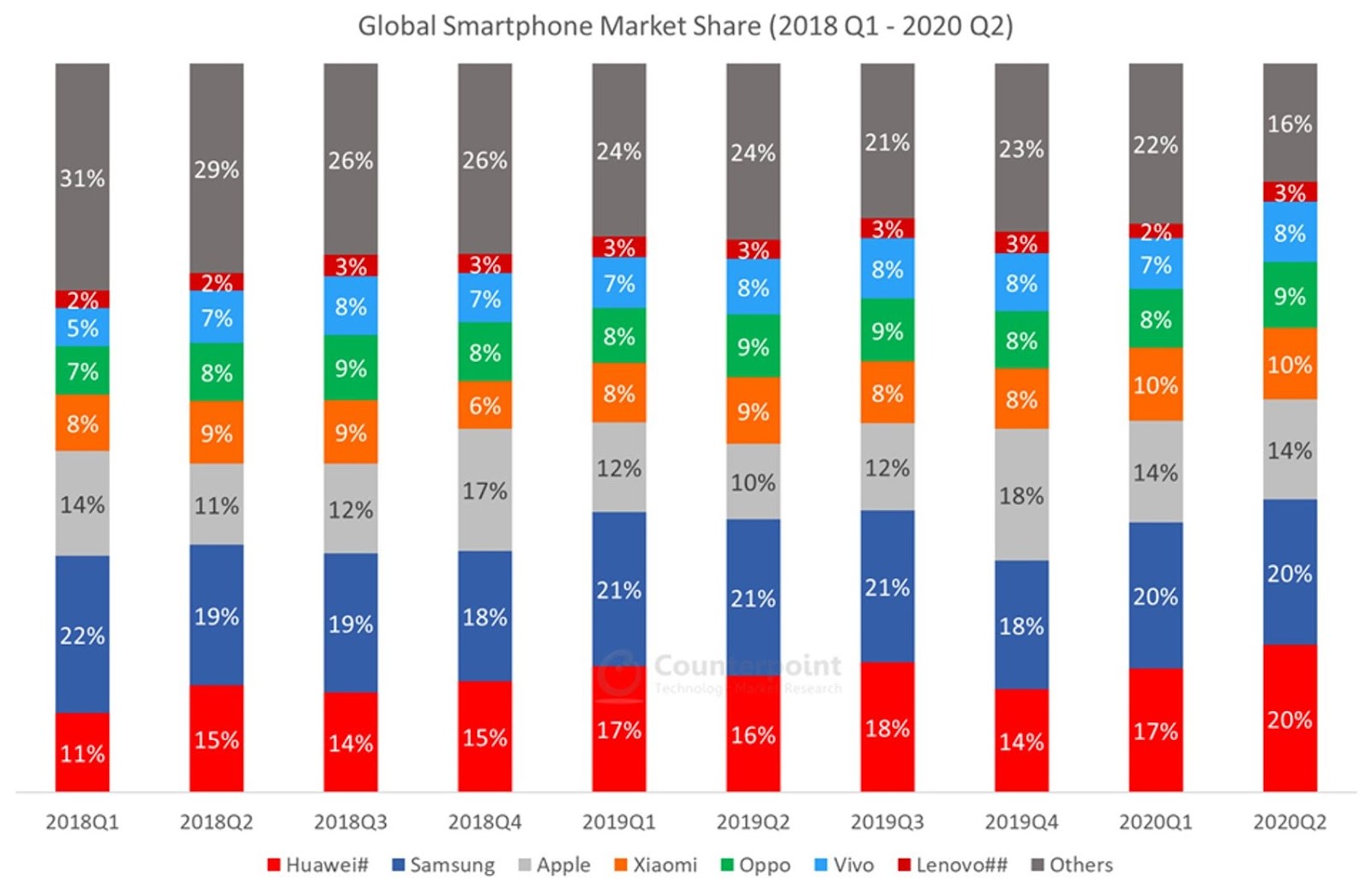

If we zoom into the smartphone segment, we see the following:

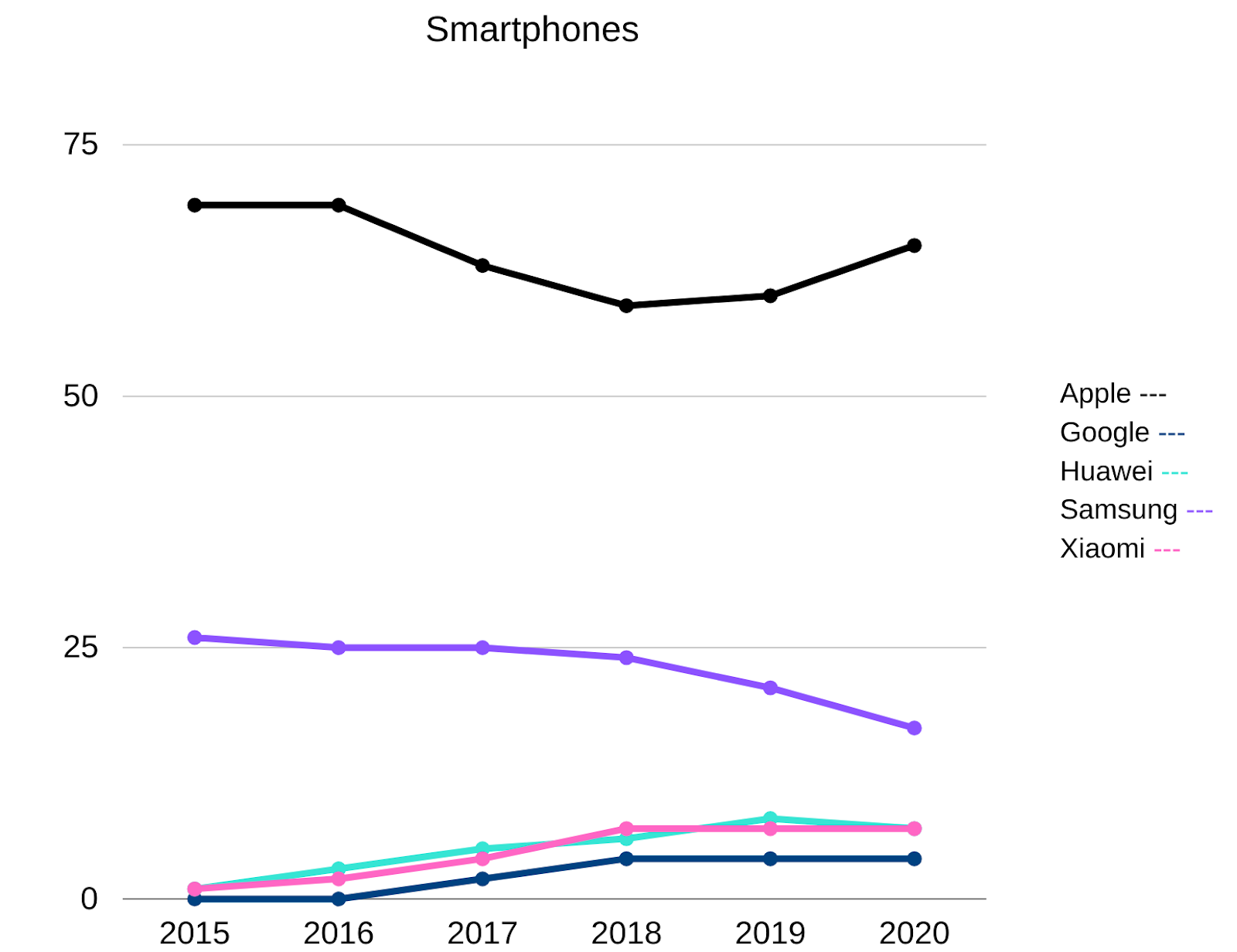

Apple’s market share has remained consistent, while there has been some volatility among Android manufacturers, with Huawei recently challenging Samsung as the market leader and Xiaomi emerging as the number three player. For the purposes of this analysis, Huawei, in particular, is an interesting story given their prominent partnership with Leica. But, as we’ll see in usage data, at least among people who care enough about their photography to share their images on stock photography sites, the most used mobile devices for photography doesn’t correlate with overall market share.

Within the camera segment, there are a few high-level observations:

The decline in the volumes of dedicated camera sales has been precipitous and has continued to drop in 2020.

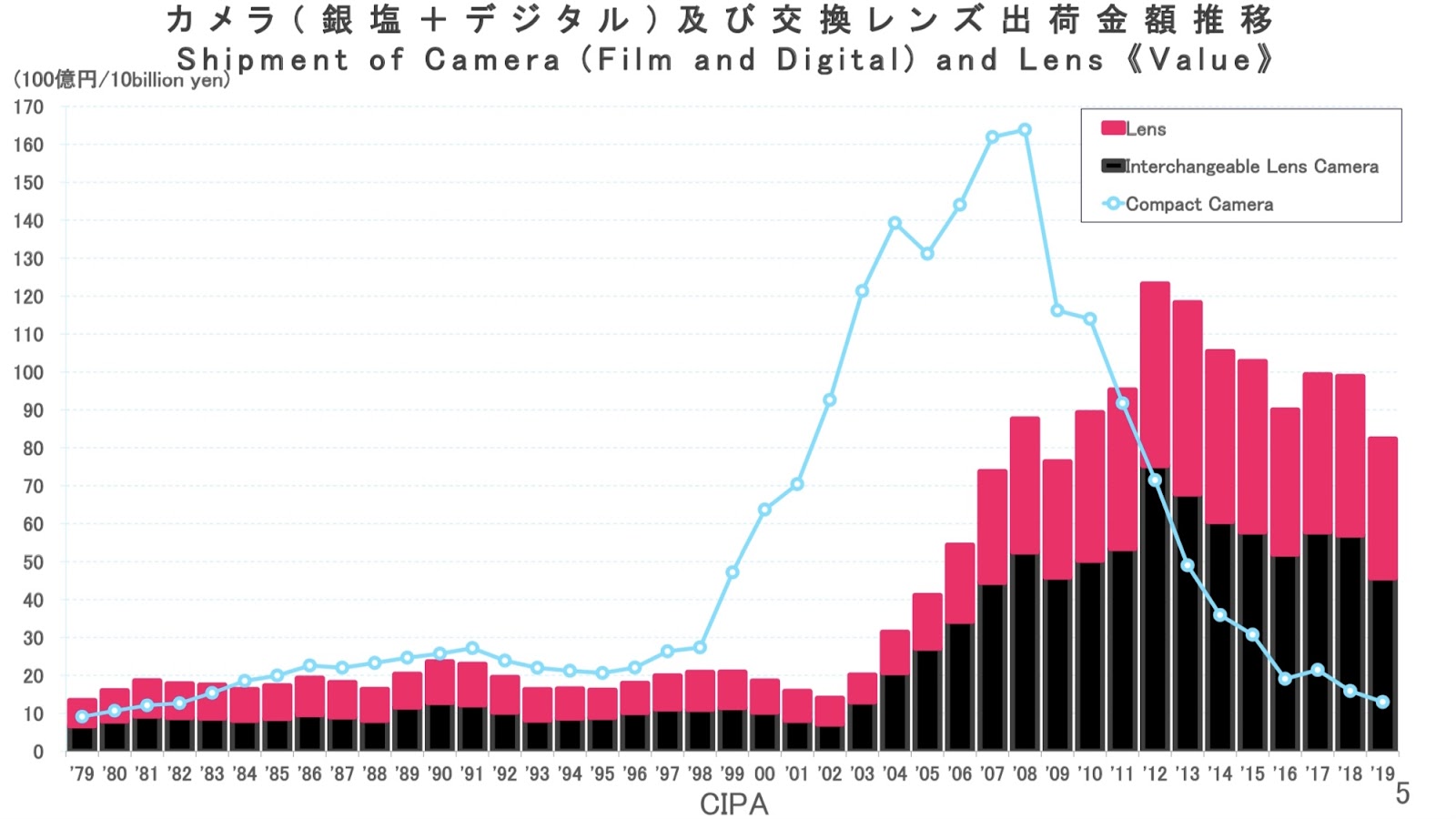

However, when looking at value there is some nuance:

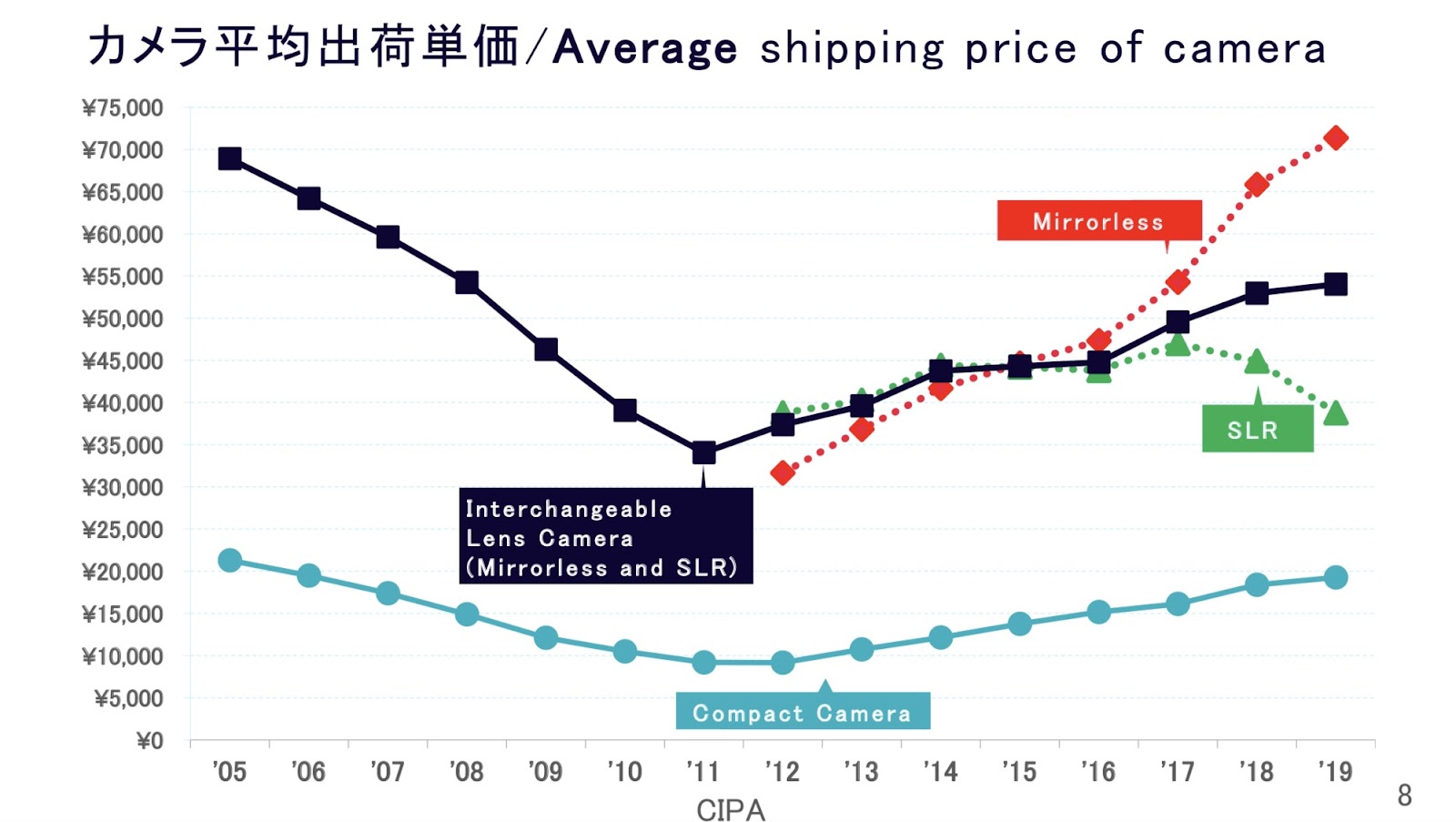

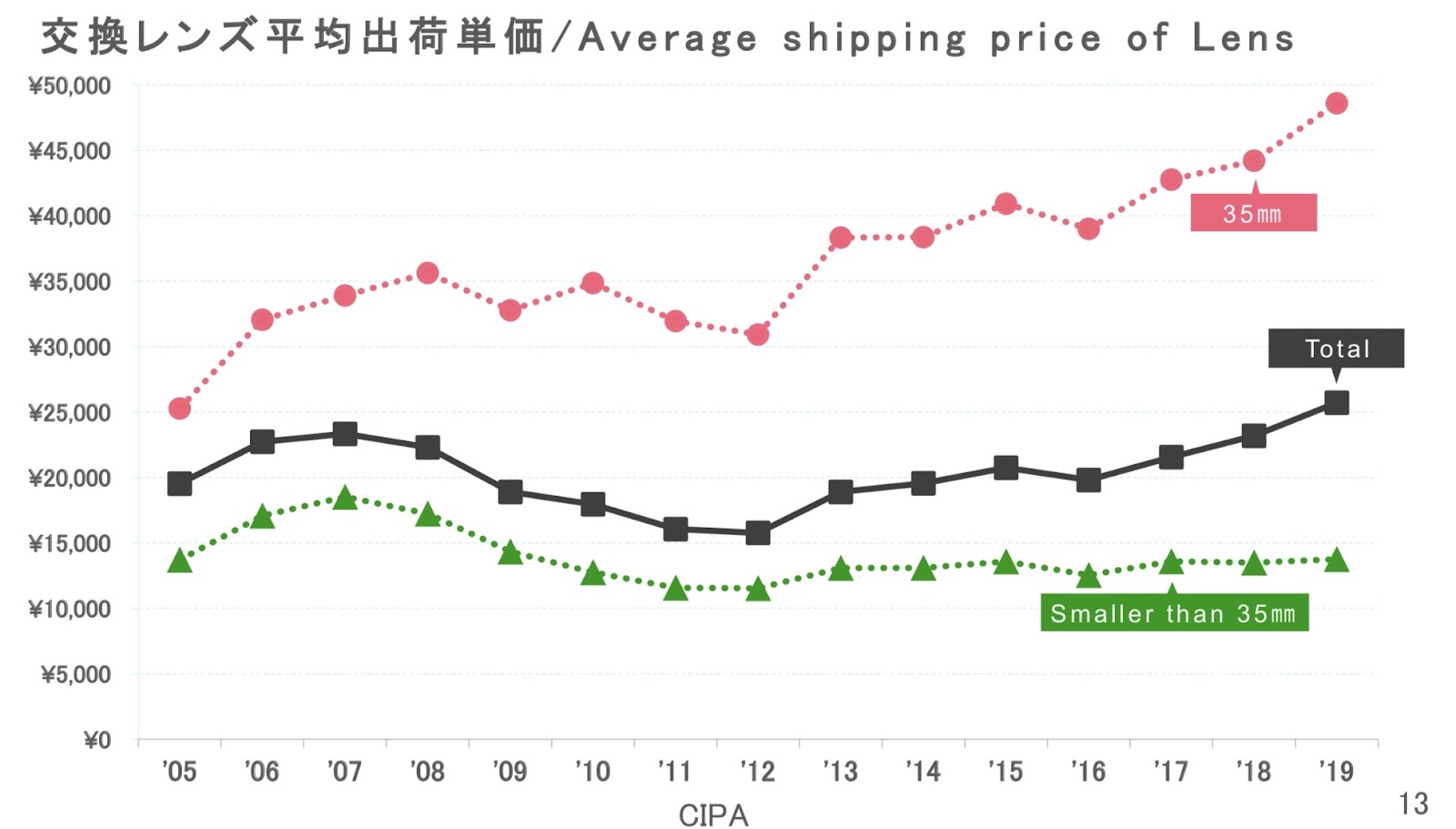

Mirrorless cameras, on average, sell at higher prices than DSLRs and the prices of lenses have been creeping up as well, driven by the proliferation of full-frame (35mm) bodies, as the following charts indicate. This has somewhat buffered the decline in the value of sales across the industry.

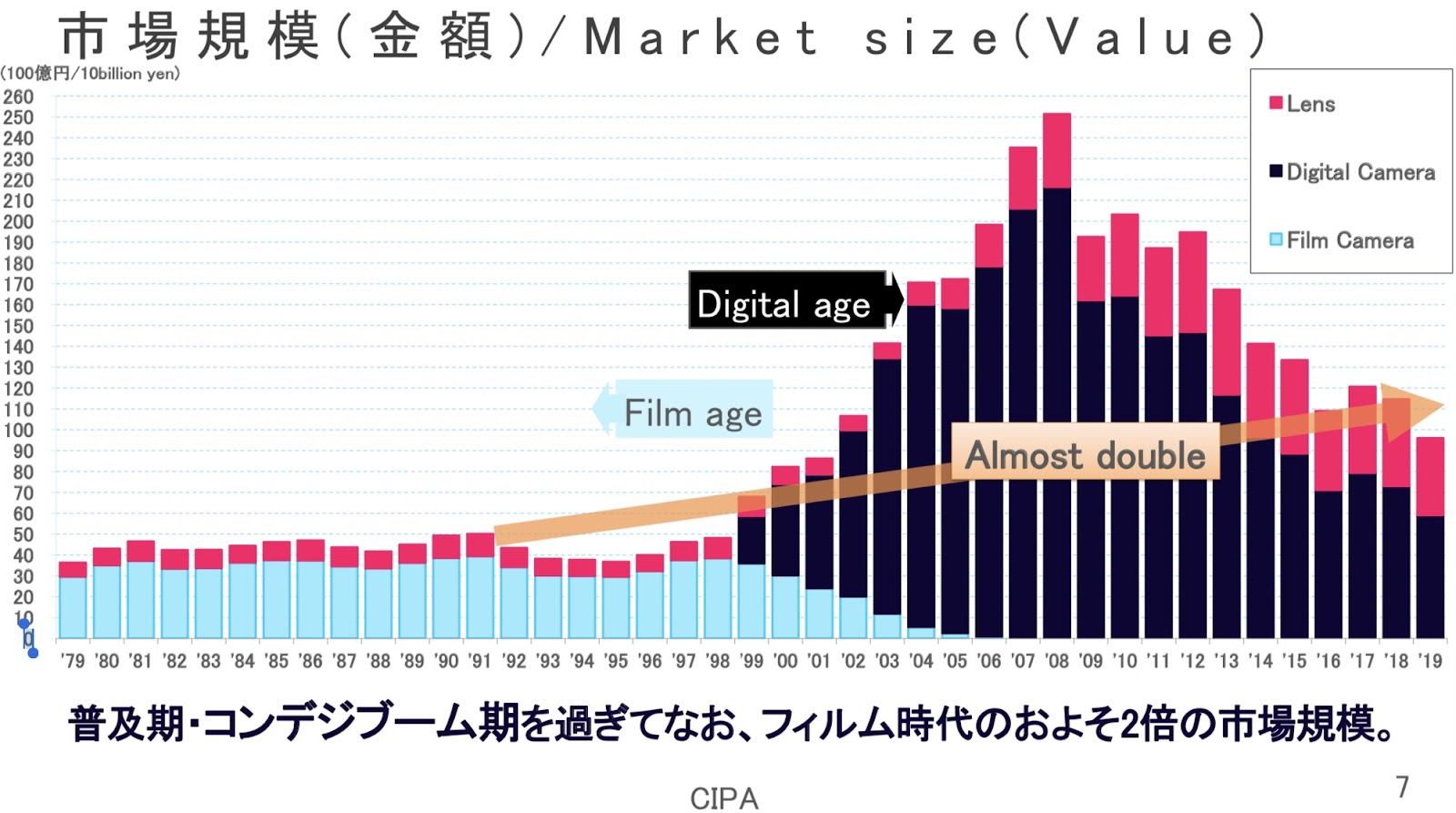

To put things into historical perspective, the digital camera market is, unsurprisingly, far larger than the film camera market ever was:

(Note: CIPA tracks only the Japanese companies, so excludes Leica and Hasselblad, but among lens manufacturers, it does include some Zeiss lenses, which are manufactured by the Japanese firm Cosina.)

A final point to highlight is related to image sensor manufacturing. Data is harder to come by for this part of the industry, but worth calling is that, among camera manufacturers, Sony dominates not only as a supplier to other manufacturers but also as a leading supplier of smartphone sensors. It is a Sony module in the iPhone, made exclusively for Apple to their spec. Sony’s main competitor among smartphone image modules is Samsung and, for cameras, it is Canon and a handful of specialised firms such as TowerJazz. Canon, however, was late to the party in terms of third-party manufacturing -sensors of their manufacture were, until 2018, exclusively for their own EOS cameras, and they used third parties for their other cameras. What matters here is that, so far, Canon has not made image sensors for smartphones and thus missed out on the major industry growth segment.

Usage

Shifting focus to camera usage, we based our analysis on data from Unsplash, a royalty-free and rights-cleared stock image site which helpfully makes their data set available upon request. We used this as it’s large (over two million records), composed of amateur and professional photographers who are serious enough to share images beyond social media, who shoot across phones and cameras and thus representative of the broader usage trends.

At the top line, in 2015, 84% of the photos on Unsplash were taken with cameras, and 16% by smartphones, so far in 2020 those taken with cameras have dropped to 75% and smartphones rose to 25%, while the total number of photos in the Unsplash data set has also grown substantially.

The composition at a manufacturer level over that time period, while not exactly volatile, has seen some interesting changes.

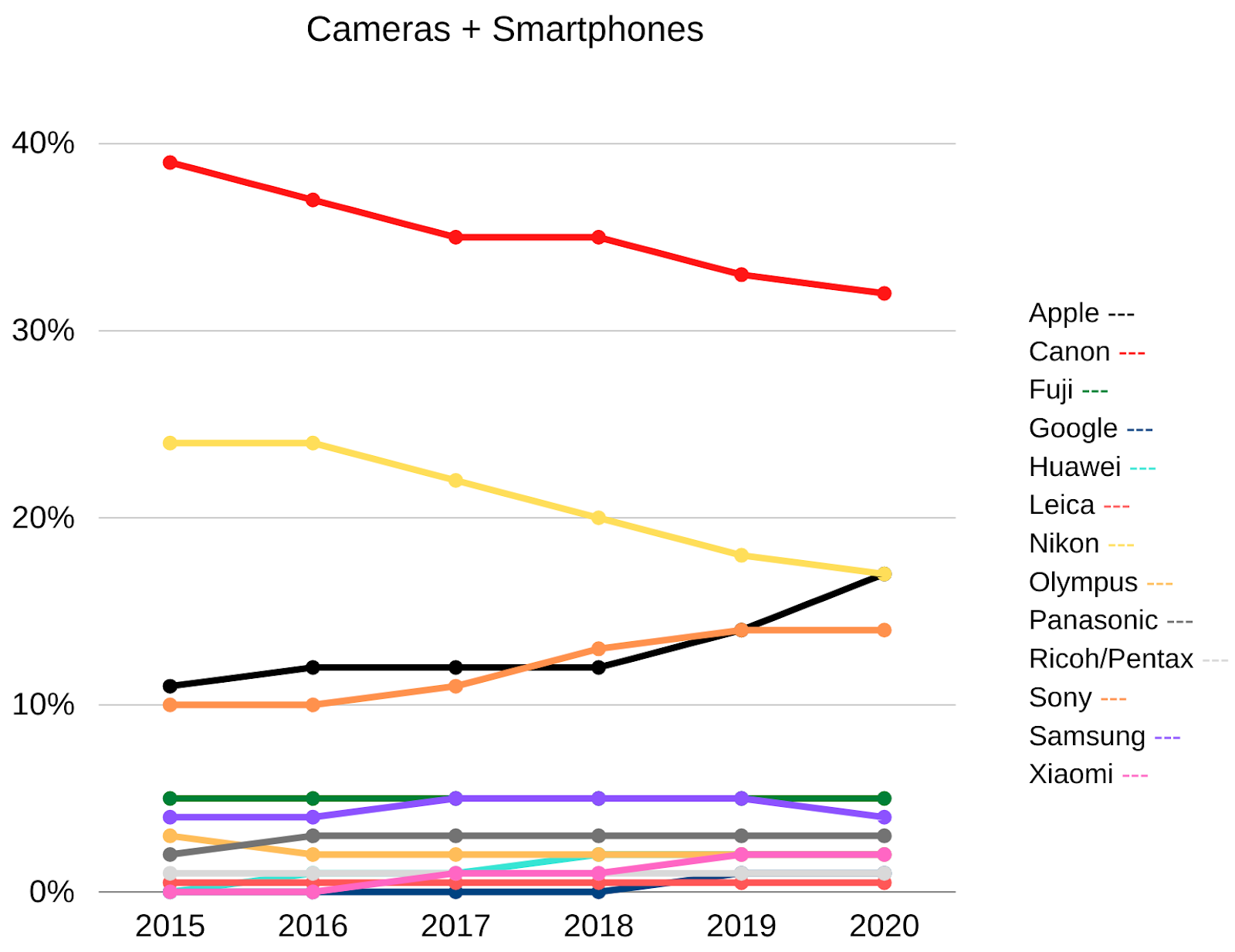

Here we see the combined usage trends across cameras and smartphones:

The big story here is the rise of Sony and Apple, mainly at the expense of Nikon and Canon, though the latter retains a dominant usage share.

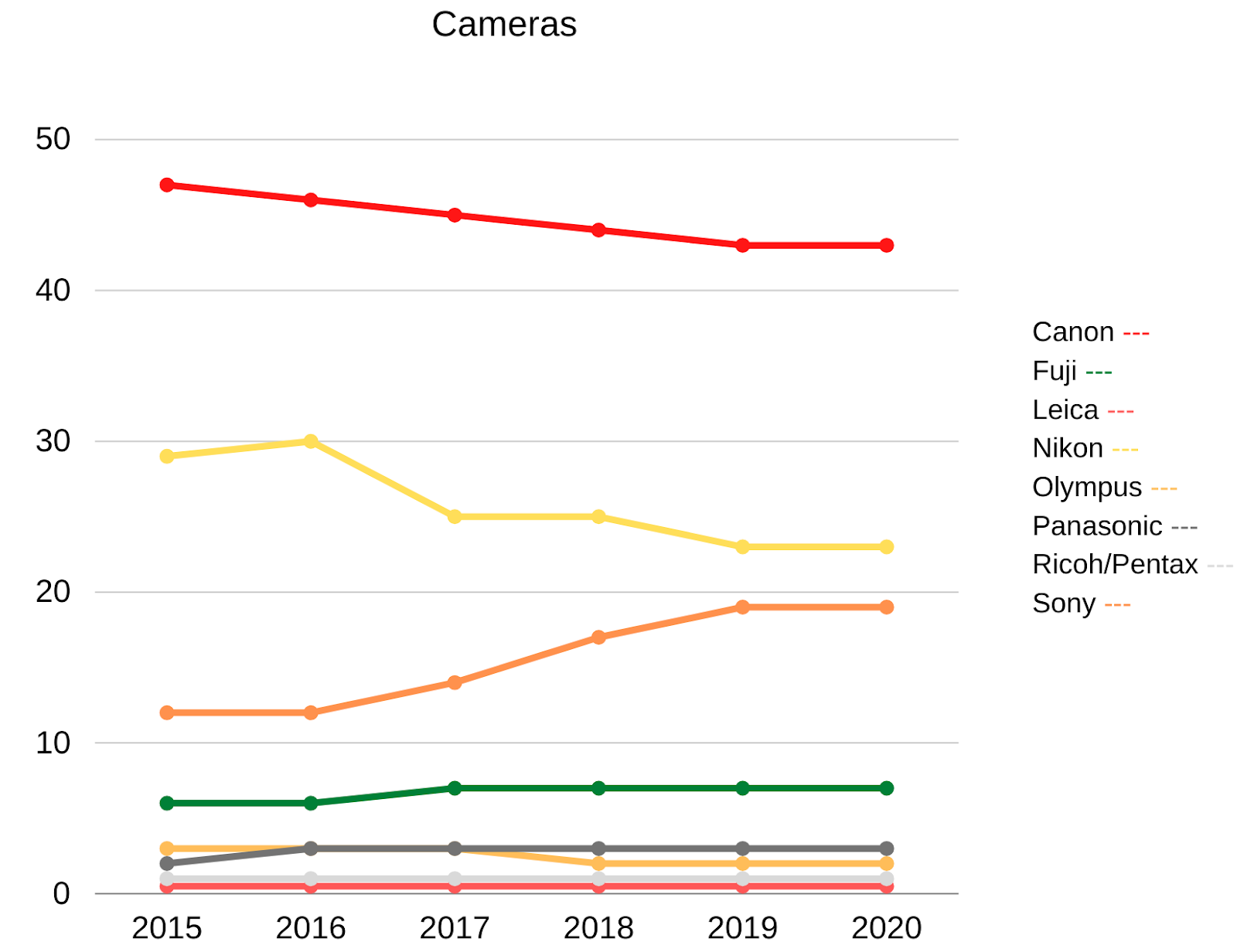

Here are just cameras:

Unsurprisingly, a similar story here but, with greater legibility among the smaller manufacturers. It’s interesting to see that their usage has been consistent over this time frame which means different things for different firms, which we look at in greater detail in the next section.

And here are just smartphones:

As alluded to earlier in the introduction of this post, usage share is starkly different from market share. Photographers have a substantial preference for Apple. Cameras and the ecosystem of photography apps on Android phones have improved significantly, and this did take some usage share away from Apple. However, it looks like Apple has regained share.

(Note: in all cases, these are relative to the brands in the consideration set. There are of course other manufacturers, but these are the ones we’re focusing the analysis on. In the case of smartphones, Google was included as they’re a major player in the computational photography space and their Pixel range has highly regarded cameras. Yet, it was interesting to see their limited usage share.)

Manufacturer Snapshots

Cameras & Lenses

(Note: while Sigma and Tamron were not reflected in the data above, given the trends in lens sales we felt it makes sense to include them in these snapshots as they’re important industry players)

Canon

- Imaging Product 2019 Revenue: $7.6 billion

- 2020 Projected Revenue vs 2019 Actual Revenue: -20%

- Imaging Revenue as % of overall Revenue (2019): 23%

- Number of ILC bodies shipped 2019: 4.16 million

- Number of new cameras:

- 2020: 6

- 2019: 7

- 2018: 7

As the largest camera manufacturer, the state of Canon reflects the state of the industry as a whole. The decline in their revenue and usage share has come at the expense of Sony and smartphones, in the photography sector that mostly means Apple. Strategically, two areas where Canon has been slow to move into appear to have compounded issues:

- Launching their 3rd party imaging sensor business in 2019. Consequently, they missed out on the rise of the smartphone, which significantly propelled Sony. This doesn’t preclude them from making smartphone image sensors in the future. Still, as we approach smartphone saturation, the initial stage of growth (billions of devices) is over and we move to replacement and upgrade cycles (hundreds of millions of devices a year, still a sizable opportunity).

- Similarly, they took their time to enter the full-frame mirrorless segment and their initial camera models (the R and RP) were met with a relatively muted response, compared to the enthusiasm for their DSLR predecessors. Canon appears to have addressed this with the R5 and R6. Their lenses for the new RF mount have been very highly regarded, which reflects the lens vs body trend noted in the Industry Overview and likely will payoff long term as a strategic bet. Canon focused their RF mount efforts early on very high-end, professional lenses such as a pair of f/1.2 primes at 50mm & 85mm, f/2.8 zooms that cover the most used focal lengths 15-35mm, 24-70mm and 70-200mm and an industry first 28-70mm f/2 – each of these lenses retail for over USD 3,000.

Despite the challenging business environment, Canon operates from a position of strength. The parent company is reasonably diversified and the imaging business itself is very large which should give them flexibility as they make the transition from DSLR to mirrorless. Taking the cue from their lens product strategy for the RF-mount, Canon is clearly positioning for the professional segment and now, with the R5 and R6 bodies, have given that customer base a viable upgrade from its beloved 5D and 6D.

Sony

- Imaging Product 2019 Revenue: $10.1 billion (includes imaging sensor business)

- 2019 Revenue vs 2018 Actual Revenue: +22% (includes imaging sensor business)

- Imaging Revenue as % of overall Revenue (2019): 13%

- Number of ILC bodies shipped 2019: 1.66 million

- Number of new cameras:

- 2020: 3

- 2019: 7

- 2018: 5

Sony defined the full-frame mirrorless segment in 2013 with the A7 and have continued to pull the industry forward with class-leading features such as stabilisation (IBIS), continuous autofocus (AF-C), realtime subject tracking, and clean high ISO for extreme low light photography. All while, they have kept their cameras remarkably compact and iterating fast to improve areas of weakness: battery life (they’re now also class leaders here) and durability. With the release of the A7C they continue to evolve, this time in terms of form factor and size.

However, the mirrorless full-frame segment is getting crowded. Canon and Nikon both now have a comprehensive range of bodies. While in absolute terms there are more (and more varied) lenses available for Sony’s E-mount, Canon and Nikon have caught up fast in the most common focal lengths (with a few unique and exotic lenses padding the range). Additionally, the L-mount alliance of Leica, Panasonic and Sigma offer another alternative, as does the medium format GFX series from Fujifilm.

Perhaps the most important aspect of their imaging business has to do with sensors. Crucially, they make the imaging sensor that Apple uses in the iPhone and consequently, there is a tight correlation between Apple and Sony’s growth. Innovation also continues in this segment of their business, with the 48 MP sensor that’s in phones such as the Huawei P40 series and the and 61 MP full-frame sensor in the Sony A7R IV (though we have yet to see it in any other cameras). On the smartphone sensor front, there has been increased competition from Samsung whose 108 MP sensor has a ready market among Samsung’s own phones and has found its way into those from other manufacturers.

Nikon

- Imaging Product 2019 Revenue: $2.3 billion

- 2019 Revenue vs 2018 Actual Revenue: -24%

- Imaging Revenue as % of overall Revenue (2019): 38%

- Number of ILC bodies shipped 2019: 1.73 million

- Number of new cameras:

- 2020: 5

- 2019: 5

- 2018: 4

Among the large Japanese conglomerates, Nikon is more dependent on their imaging business than any of the others and thus most at risk to volatility, given current trends which have exacerbated an already challenging situation.

Nikon also has no image sensor business, nor any significant industry partnerships and had, until the launch of their Z full-frame mirrorless range in 2018, also not focused much on the video segment.

From a product strategy and execution perspective, however, there is little to fault with the Z series. It combines Nikon’s justly famed ergonomics and familiar DSLR menus with industry’s shortest flange length, theoretically future-proofing their lens lineup, and competitive technology and features including nice to haves such as focus stacking. An emphasis on image quality and low-light performance remain cornerstones of the system, and the Z6 and Z7 were the right cameras to launch with and updates are coming soon. They were followed by the slightly retro, but accessibly priced, APS-C based Z50 and, most recently, the very well received full-frame Z5, which drops some of the Z6’s features to compete more effectively on price.

It’s a similar story in terms of lenses, where the only glaring omission is an affordable 70-200mm zoom lens -not dissimilar to Canon’s RF-mount strategy, Nikon has emphasised expensive pro-grade optics, releasing an f/2.8 telephoto zoom before an f/4 or variable aperture model. Otherwise, they cover the range of focal lengths with zooms and small-ish, fast-ish primes, having recently added a high-end prime with the 50mm f/1.2 and prior to that a showcase for what’s possible with the Z-mount in the form of the Noct 58mm f/0.95. At the time of the Z50 launch, they also released three very affordable, compact, APS-C zoom lenses – a 16-50 f/3.5-6.3, a 24-50mm f/4.5-6.3 and 50-250mm f/4.5-6.3 that, when paired with the high-res Z7 make for a very lightweight system that still offers >20 MP even in crop mode. The first party FTZ adapter gives Nikon users full compatibility with legacy AF lenses (screw-drive models function MF only) to plug the few gaps in the native Z-mount range — presently speciality macro and very long telephoto lenses.

With this solid foundation, the balancing act Nikon has to play is between divesting themselves of their legacy DSLR business, while maintaining support for their users and, at the same time, aggressively ramping up their mirrorless business in a highly competitive space within the context of industry-specific and broader business challenges. Their recently announced Z6 II and Z7 II speak to this, as they take an iterative approach by incorporating market feedback (i.e. dual memory card slots), improve key features (i.e. autofocus) but don’t try and fix what’s not broken (i.e. ergonomics).

Fujifilm

- Imaging Product 2019 Revenue: $3.6 billion (includes a/v production equipment)

- 2019 Revenue vs 2018 Actual Revenue: +1%

- Imaging Revenue as % of overall Revenue (2019): 16%

- Number of ILC bodies shipped 2019: 0.5 million

- Number of new cameras:

- 2020: 3

- 2019: 5

- 2018: 7

While not at Sony’s scale, Fujifilm’s camera sector has been another bright spot in the industry. Their fixed lens X100 series — as the only large sensor compacts other than the Ricoh GR, Leica Q and ageing Sony RX1 ranges — have a dedicated fanbase. Their high-end mirrorless X-T3/4 were both very well received and generally viewed as being legitimate APS-C based alternatives to Sony’s A7x and Panasonic MFT based GH5/G9 models, as among the top cameras for both stills and video. They’ve also placed a reasonable bet on the professional segment with their mirrorless medium-format GFX range where their only direct competitor is Hasselblad. However, large sensor full-frame models such as the Sony A7R IV, Leica SL2, Nikon Z7 and Canon R5 address similar audiences.

On the lens side of their business, as their range covers almost every conceivable use-case and focal length, they’re now venturing into the exotic realm with products like the Fujinon f/1.0 50mm lens, the first autofocus lens at that aperture.

Panasonic

- 2019 AVC Business Revenue: $6.3 billion (includes all a/v and communication products)

- 2019 Revenue vs 2018 Actual Revenue: -6%

- AVC Business Revenue as % of overall Revenue (2019): 8%

- Number of new cameras:

- 2020: 3

- 2019: 7

- 2018: 6

Panasonic do not appear to report detailed segment revenue or unit shipments for their photography business, but this reflects the reality that, as an $80 billion corporation, cameras are a tiny part of their business. Historically, a significant part of their strategy in the sector has relied on partnerships, with Olympus for the micro-four-thirds (MFT) system and Leica for lenses as well as bodies -the Leica D-lux, C-lux and V-lux models are based directly on Panasonic models whereas internal components from the Panasonic S1R have found their way into the Leica SL2. More recently, Panasonic became one of the three members of the L-mount Alliance, along with Leica and Sigma.

With the sale of Olympus’ camera business to JIP (more below) the future of MFT is less clear than it had been previously, though the pace at which Panasonic was releasing MFT bodies had been slowing for some time. Perhaps this was as a result of their investment into full-frame, of which they’ve released four bodies in two years. They’ve announced that they will position MFT as tools for video creatives and vloggers

For the L-mount, Panasonic’s lens roadmap includes some much-needed small, fast, reasonably priced primes.

Based on statements in the conglomerate’s annual report that every business unit must drive profitable growth, which is likely going to be somewhat of a challenge for the photography unit and as such casts some doubt over Panasonic’s long-term interest in the space.

Olympus

- 2019 Revenue: $421 million

- 2019 Revenue vs 2018 Actual Revenue: -10%

- Imaging Revenue as % of overall Revenue (2019): 6%

- Number of ILC bodies shipped 2019: 0.33 million

- Number of new cameras:

- 2020: 2

- 2019: 5

- 2018: 1

Olympus’ parent company (who also make medical and other industry-specific equipment) have exited the camera business, selling the assets to JIP (Japan Industrial Partners), who struck a similar deal with Sony in 2014 for their VAIO computers business unit. There have been conflicting reports about whether JIP has licensed the Olympus and OM-D brand names and so it is unclear what branding the cameras will carry going forward.

With the expectation of a few rugged, compact cameras, Olympus has been all-in on MFT. When the format was at its peak, roughly between 2013 and 2017, when Olympus released the E-M1 Mark I and II, and Panasonic the GH4, GH5, GX8 and G9, Olympus were arguably as, if not more, innovative as Sony from a technology perspective. They were innovators in IBIS, AF-C, continuous shooting rates and performance while also offering ergonomic, durable bodies and top-notch lenses.

Evidently, this was not enough. We can see from our usage analysis that all of this innovation did not translate into share gains among photographers; whereas it did with Sony. Perhaps this was a function of the limits of MFT as a platform or maybe just the struggles of competing against much larger companies such as Canon, Nikon and Sony -likely a combination of the two.

It is also unclear what JIP will do with Olympus in terms of product strategy. If what they’ve done with VAIO offers any clues, we can expect one mainstream line (think either E-M10 or E-M5, but not both) and more advanced one (think E-M1), with nothing focused on pros (think end of the line for E-M1X). However, it’s not inconceivable to see the entire E-M1 line deprecated and the E-M10 become the mainstream line and the E-M5 the advanced one; or the less likely alternative of making the status quo: basic (E-M10), advanced (E-M5) and pro (E-M1).

Ricoh/Pentax

- Doesn’t report details of imaging division

- Number of new cameras:

- 2020: 1

- 2019: 2

- 2018: 3

While Ricoh/Pentax recently reaffirmed their commitment to photography products, and specifically to APS-C based DSLRs, it is hard to believe that there is much of a future for them, even as a niche player. No matter how good their products are, it is clear at a macro level that the total addressable market for dedicated cameras is constrained. Consumer demand, and supply from other manufacturers, has shifted to mirrorless. It is unlikely that their margins support the ability to carve out a meaningful niche for themselves in the way that Leica has, thus their prospects are unclear.

While it’s not inconceivable that autofocus, interchangeable-lens digital cameras with optical viewfinders will experience a renaissance similar to what 35mm film cameras have allegedly experienced — the fact that Nikon recently announced end of life for their last film SLR, leaving Leica as the last dedicated camera company making new film camera, indicates that the film renaissance might be overstated — it seems like a long and lonely journey for Ricoh/Pentax between now and that potential future.

The one stand out in Ricoh’s line-up is the GR III, the most recent iteration in a long line of large-sensor compact cameras that, similar to Fujifilm’s X100 series, have a cult following, particularly among street photographs who appreciate its discreet package, sharp lens, snap focus feature and high quality sensor. While the 2018 update to the GR III brought a new 24MP sensor (up from 16MP in the GR II), IBIS, USB-C, upgraded autofocus, all in an even smaller package, Ricoh has put little marketing support behind it, nor has there been any word of further updates.

Leica

- Privately held

- Press coverage indicates 2019 revenue of $475m

- Number of new cameras:

- 2020: 2

- 2019: 4

- 2018: 5

As the definition of a niche player, Leica represented a potential model for other manufacturers to emulate. Their unique asset, however, is their brand and a disciplined business that likely yields margins that are well above industry norms.

Given that they make many of their products in Germany and Portugal, their costs are also higher than their peers, but this is factored into the business model. They’re perceived as a heritage brand, but this doesn’t give them credit for where they have innovated: industrial design, ergonomics, user interface and experience. Their flagship SL2 is competitive with flagship models from other manufacturers on every dimension except autofocus, and they continue to build products such as the M-10 series for their traditional loyalists and those seeking a different type of photography experience. Their partnerships with Panasonic and Huawei give them access to technology and, in the latter case, participation in the growing smartphone market where, assuming that there is some kind of unit-sales based revenue sharing deal in place with Huawei, the growth of Huawei’s market share might have delivered some nice additional income.

If Leica has a weakness, it is their reliance on these partnerships. In Panasonic’s case, should they start to reduce their level of investment in their camera business this could potentially leave Leica exposed on the technology side. Emerging areas such as computational photography that underpin advancements in autofocus (where Leica is already borderline non-competitive) is one example where Leica might need to invest alone, whereas they’ve likely shared investment with Panasonic to date. Huawei is a partner who offers a potential hedge against this exposure, but they’re having their own, well documented, challenges.

One example that Leica could potentially emulate, should it choose to update the TL series, for example, is that of the Zeiss ZX1, which has built its operating system around Android and runs Adobe’s Lightroom directly on the camera itself for on the go editing.

Another partnership that has a significant bearing on Leica’s future is the L-mount alliance with Panasonic and Sigma. Two years in, it has been perceived as successful, with a range of bodies that, with the recently released Panasonic S5, addresses most use-cases and price points and a comprehensive range of lenses that do the same. With this solid foundation, the challenge ahead for the alliance will be their ability to coordinate strategically around products against more integrated competitors in the form Canon, Nikon and Sony. Leica’s role in the alliance is relatively straightforward as the maker of high-end lenses — a good segment of the industry to be in, as validated by Canon’s RF-mount strategy.

Sigma

- Privately held

- $350m 2019 revenue

Their dabbling in ergonomically challenged camera bodies aside, Sigma have been in one of the two industry sweet spots: lenses (the other being image sensors).

Though Sigma does make a couple of very long telephoto lenses for the Canon EF and Nikon F DSLR mounts that retail for over USD 25k, they typically do not compete in the ultra-high-end (price point) range. Instead, they strive for a balance between price and quality with their Art series and add in compactness with their Contemporary range. Their Sports range is comparably priced to similar first-party lenses.

This is also the role that they play in the L-mount Alliance, with Leica and Panasonic: to cover the range of focal lengths with quality, competitively priced lenses while Leica covers the high-end and Panasonic plugs specific gaps. Sigma makes half (22 out of 44) of the currently available L-Mount lenses

Sigma has also released one L-mount camera body, the fp which remains, even following Sony’s launch of the A7C, the smallest full-frame ILC on the market, but accomplishes this with the omission of IBIS, a mechanical shutter, an EVF and somewhat compromised handling.

Tamron

- Photographic Products 2019 Revenue: $420m

- H1 2020 Revenue vs 2019 Actual Revenue: -33%

- Photographic Products Revenue as % of overall Revenue (2019): 70%

Much of what’s true about Sigma is also true about Tamron, except that they are a larger company and, as a publicly listed one, more conservative/disciplined around product development, being solely focused on lenses.

Tamron supports fewer mounts than Sigma -Canon EF and Nikon F DSLR, mainly Sony E on mirrorless -and have been slower to grow their mirrorless range, partially constrained by the fact that Nikon have yet to open up their Z-mount to third parties.

Smartphones

It’s useful to look at the mobile unit revenue for the major smartphone players to give a sense of the orders of magnitude of difference between camera sales and smartphone sales. Very nearly everyone does have a reasonable camera with them at all times. This has led not only to a democratisation of photography in a way that point and shoot cameras never did but to an explosion of pictures shared and a new vernacular, whereby images have replaced words for basic communication.

The smartphone has had not just the obvious profound impact on society, but also on the role of the photographer and photography, whether as a profession, hobby or art form.

Apple

- 2019 iPhone Revenue: $142B

- 2019 iPhone Revenue vs 2018: -13%

The iPhone has a substantial lead in usage share among photographers compared with other smartphones. Unsurprisingly, particularly with their Pro model, Apple put the iPhone photography features front and centre in their marketing. An entire ecosystem of photography apps and accessories has sprung up around the iPhone, enabling it to operate at pro levels (see the Shot with iPhone campaign).

Apple has just announced the iPhone 12 which continues to push forward smartphone photography technology in the same way that its predecessors have. Each year it seems like we’re approaching the limits of what can be done in terms of photography on a phone, only to see the boundary of those limits pushed out further the next year. This year saw the surprising evolution on the Pro Max model of an imaging sensor that’s 47% larger than previously, which promises significantly better low light performance, which has been an area where phones have relied on software rather hardware to compete with cameras. Also upgraded is the stabilisation system (more hardware based improvements for low light situations) and, again on the Pro Max, a new 65mm equivalent (up from 52mm) telephoto lens, which also benefits from the improved stabilisation. On the software side Apple now offers the ability to edit HDR images post capture in the native Photos app and, later in the year, will bring Apple ProRAW to these new phones. Their version of RAW, it takes advantage of computational photography (such as HDR) at time of capture, while offering greater flexibility in editing.

Samsung

- 2019 Mobile Products Revenue: $87B

- 2019 Mobile Products Revenue vs 2018: +6%

While Samsung does their due diligence in touting the photography features of their new phones at launch time, they haven’t made it quite the central part of their marketing in the way that Apple, Huawei and Google have. They’ve seen their usage share diminish in the face of Apple, Huawei and Xiaomi.

Unlike other smartphone manufacturers, Samsung make image sensors as well, where they compete with Sony. In addition to their own phones, their sensors are seeing broader industry adoption. Notably, Xiaomi’s flagship Mi 10 and Mi Note 10 both use Samsung’s flagship 108 MP sensor.

Huawei

- 2019 Consumer Products Revenue: $69B

- 2019 Consumer Products Revenue vs 2018: +33%

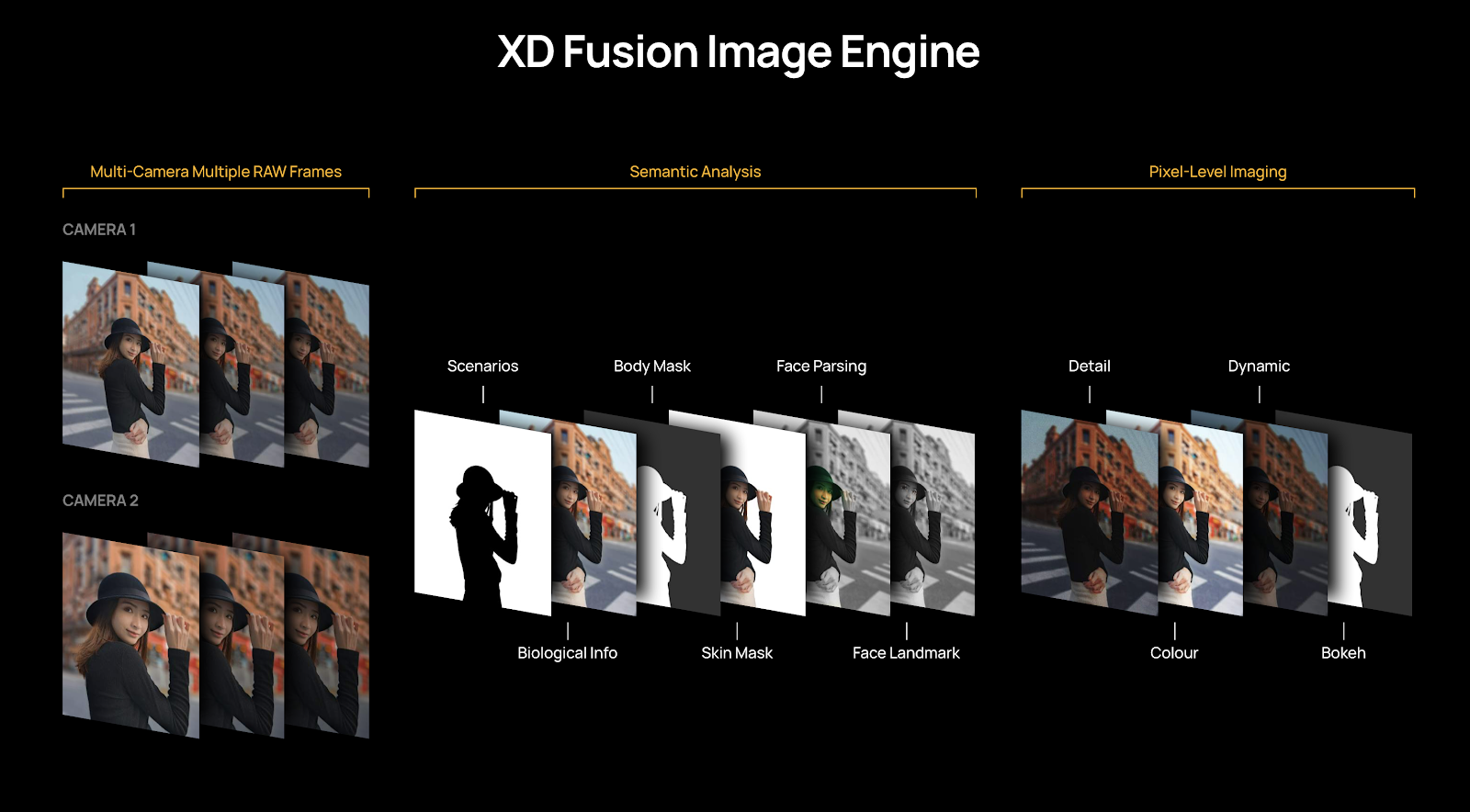

Central to Huawei’s photography bonafides is their partnership with Leica, which has helped with both branding and the optical quality of their camera module. From a software perspective, Huawei has also emerged – along with Apple and Google – as a leader in computational photography; their emphasis (illustrated in the graphic above) has been on advanced scene analysis and automated settings to match the scene. This is complemented with a fully manual mode aimed at pro photographers.

Xiaomi

- 2019 Total Revenue: $30B (does not report segment revenue)

- 2019 Total Revenue vs 2018: +15%

Xiaomi has recently started their marketing push beyond China, India and emerging markets into Europe and the UK, hence the brand is somewhat less known, but as their market and usage share indicate, they are a major player. Their flagship Mi 10 and Mi Note 10 models both use Samsung’s 108 MP sensor, which put them in the upper echelon of photography oriented smartphones.

- 2019 Other Revenue: $17B (includes all hardware and subscriptions)

- 2019 Other Revenue vs 2018: +21%

While the usage share of Google’s Pixel has yet to catch up with their photographic ambitions, they continue to be a leader in computational photography. Initially, their focus was on portrait mode, lowlight and HDR, but this has subsequently expanded to AF-C, subject recognition and tracking. Like Apple, their emphasis is on simplicity and automation. While the Android photography app and accessory ecosystem aren’t as extensive as the iPhone’s, key companies such as Filmic and Moment do support the Pixel, making it a viable platform for photography.

Conclusion

The defining photography industry trends of the past decade – namely the rise of the smartphone as a viable photographic tool and the transition from DSLR to mirrorless – continue to shape the industry today. This has crowned new champions, notably Sony, and made life difficult for legacy players such as Nikon and Olympus.

Canon, Sony, Fujifilm and Leica appear to be well placed to navigate the choppy waters ahead and, assuming they can stabilise their balance sheet, Nikon can be added to that list. The road ahead is less clear for Panasonic, Olympus and especially Ricoh/Pentax.

In the short term, robust lens sales, buoyed by new purchases as users continue to make the shift to mirrorless systems, will support Canon, Nikon, Sigma and Tamron revenue, while Sony continues to gain share.

While smartphone adoption appears to be approaching saturation, there is still the replacement rate and upgrade cycle to account for (hundreds of millions of annual device sales). It offers both an opportunity for image sensor sales, and Canon could still enter this lucrative market and cooperative projects. Partnerships similar to Leica and Huawei’s (would a Nikon branded camera array help an emerging smartphone manufacturer’s bid for photographic credibility?) and will spawn continued advances in computational photography that could find their way into cameras.

One aspect we haven’t commented on is form factor innovation.

The 2013-2014 time period produced what amounted to a series of mostly failed experiments such as Sony’s “Connected Lens” Q-Series, Samsung’s Galaxy Camera, Nokia’s Lumia 1020, Panasonic’s CM1 and the Leica T. A common theme among these devices was the attempt to fuse elements of dedicated cameras with the emerging user interface and experience paradigms of smartphones. While vestiges of these experiments live on — touchscreen-based interfaces are now ubiquitous among cameras, as are smartphone apps that extend the functionality of cameras to smartphones, which indicates an increasingly symbiotic relationship between the two. Smartphones themselves, notably models from Huawei and Samsung, offer “Manual” or “Pro” modes within the default camera app (though, notably, this is something that Apple and Google have eschewed).

While it might seem like an unlikely time to renew these experiments — though we have seen the long-delayed, believed-to-be-vaporware Zeiss ZX1 finally go up for pre-order — the fact that smartphone adoption is close to saturation makes it feels like there may be scope of opportunity.

As noted above, another potential direction that we’ve seen is the incorporation of computational photography, which has primarily been the domain of smartphones, into cameras. In smartphones, it has been used to offer the advanced features of cameras, such as portrait modes that simulate the shallow depth of field of wide aperture lenses and full-frame sensors, and for HDR, stabilisation and low light photography.

More relevant to camera-based photography is subject detection and tracking to support advanced AF-C. Initially, Olympus and more recently Canon and Sony, the latter of which has started to share technology between their cameras and smartphones, have been leaders in this space. In the realm of autofocus technology, computational photography is increasingly becoming table stakes and without significant investment into the space, Nikon, Panasonic and Leica risk being left behind. It would be a benefit to Leica if they could tap into their partnership with Huawei to incorporate such technology into their mirrorless cameras.

For the sake of speculation, it would be interesting to see Leica keep the T/TL series alive with a TL3 that builds on the touch-based user experience and adds the latest Huawei technology for scene detection and autofocus.

While that’s unlikely to happen, what we likely can count on is, despite a challenging business environment, continued refinement of cameras that bring us ever closer to — if not quite precisely to — the perfect photographic device. Autofocus and scene detection will improve. Automation combined with manual overrides will give photographers ever more fine-grained control over image capture and editing. Image resolution will continue to get higher, already impressive high ISO/low light imaging will get even more impressive.

These are the things we can count on. What we don’t exactly know, if which are the companies that will bring these advancements to us.

Sources

- Company annual reports for Canon, Sony, Nikon, Fujifilm, Panasonic, Olympus, Apple, Google, Samsung, Huawei, Sigma, Tamron and Xiaomi

- Kleine Zeitung for Leica’s revenue

- PetaPixel for state of the image sensor industry in 2019

- Canon Rumors for Canon’s entrance into the image sensor business

- 1 million row sample of Unsplash’s data set for camera usage

- CIPA annual reports for overall industry trends

- DPReview’s Camera Database for number of camera bodies released by year

- PetaPixel for 2019 ILC body unit shipment data

- Counterpoint for mobile industry market share data

- Facebook Ads Manager for iOS vs Android market share (selected countries representing 1.5 billion Facebook users)

Nikon has not “announced end of life for their last film SLR”. There is a change of parts for European models that might be causing some confusion. But the Nikon F6 is still a current camera. It is made in periodic batches.

The Nikon F6 is one of the most impressive film cameras ever made, and let’s hope its production continues for a long time still, even if like some of the others here, I have a liking for mechanical film cameras.

FWIW, B&H and Adorama both have the Nikon F6 on backorder but it is definitely not listed as Discontinued yet. Although I have no experience with the F6 I also hope that they continue to make it. I very much would like film to survive. In the US the Leica MP is pretty much unavailable most of the time. Your only chance of obtaining one it to put yourself on a waiting list. The Leica M-A seems to be more readily available.

The M-A, with no light meter, is a bit of self-flagellation too far for my taste. If I were to buy a new film camera, I’d definitely go for the MP. But, then, I have a 16-year-old MP which cost a lot less than a new one and performs just as well. It is worth more than I paid eight years ago. But the same wouldn’t be the case for a new MP. So second-hand rules, IMHO.

There is something appealing about the purity of no light meter in the M-A, but it is also easy enough to use the MP that way. The MP is my choice because of the black paint on brass finish; the only camera Leica still offers with this finish. Unless they have standardized in later production, the silver chrome also has a different appearance on the MP versus the M-A.

I don’t know if there any differences in the internal mechanical parts of the MP and M-A. I am assuming that the shutter speed arrest mechanism is the same in both, from the Black Forest manufacturer that Leica has used for decades.

I don’t own a film Leica so I have been eyeing the MP for a while. The current price (after the tariffs) of $5,295 is a bit too steep though I find. I do own a Contax G1 which is really nice as well so I will probably stick with that unless I can find a reasonably priced used MP.

From what I have seen the Contax G lenses are really nice optically. Of course, people might have rendering preferences between Zeiss and Leica, and the Contax G system might not have the mechanical satisfaction of Leica, but it seems capable of very good images.

I am not usually a proponent of taking lenses out of their original system (like how many Leica R lenses have been taken and rehoused for cinema, leaving fewer for photographers), but it is interesting that Skyllaney Opto-Mechanics is doing very high quality conversions of Contax G lenses to Leica M mount with rangefinder coupling.

Between speculation, supported by communication that some dealers claim to have received from Nikon, Nikon’s more broadly stated focus on product line consolidation and high-end cameras, and the lack of available stock, these all point to the likelihood of it being officially discontinued soon.

Overall it’s a bit of a footnote to the post as a whole.

For film cameras, what would be more interesting to look at for the current state is second hand sales and output of processing labs, but to my knowledge no reliable data exists here.

Like you say, film cameras are overall a footnote on the camera industry now. But it is interesting to note that besides the cameras already discussed and technical cameras (where there are still film capabilities), there is at least one more SLR system film camera available new. DW Photo is still offering sales and service of the Rolleiflex Hy6 mod2 camera with 6×6 rollfilm magazine and a range of lenses.

I think B&H and Adorama get batches maybe twice a year. They seem to sell out pretty quickly after they arrive. They are both usually pretty quick to change something to “Discontinued” instead of “More on the way” or “On backorder”, when that is the case.

The last news item about the F6 on Nikon’s Japanese website is 15 July 2020 about the part change to comply with the RoHS directive.

Very well-researched article and an excellent read. Thank you for putting this together! Reading this article from my very own selfish point of view. I own mainly Canon (R), Leica (M9,S2,SL,T,TL2,CL) and Hasselblad (X1DII) gear. I am not worried about my Canon gear. Canon are IMHO doing great. The RF glass is fantastic as well. I am also not worried about Hasselblad (though a lot of other people seem to be…) . The X1D II produces wonderful files, the 907X as well on top of being pure eye candy. I am less confident about Leica though and that lack of confidence is mostly driven by the way they have run their non-FF systems. The Leica S went from a very innovative and promising system to a complete commercial failure with a resale value that is close to zero. The APS-C system after 3 years of non-investment risks going the same way. The TL2 doesn’t even get firmware updates anymore. This is really not good for customer confidence. I hope Leica proves me wrong with the CL2 but my guess would be that they will do the strict minimum to keep the system (kind of) going for another 3 years, ie. same sensor, IBIS, no new lenses. Again I hope to be proven wrong.

Thanks!

Glad to hear that you’re so positive about Canon R, I haven’t had the chance to hear from many real users (having only read reviews) and have been very tempted by the R5.

I debated including Hasselblad in the analysis but beyond the 2017 investment by DJI (a good thing for Hasselblad’s long term prospects, assuming DJI maintains investment) information was scant. And their usage share from the Unsplash data was, unsurprisingly, tiny.

Agree re Leica, which was one of the surprises for me that resulted from the analysis. I went in thinking that they were very stable, with a solid foundation for the future. But the exposure to risk from their partnerships stood out to me, which the article notes. Hadn’t considered it from the perspective of product, but what you’ve highlighted does indicate that there’s some work to there, too.

My read is that they’re pruning the product lines to prioritize success and minimizing risk from experiments, with a clear preference for full-frame. That means prioritizing the Q, SL and M series at the expense of the TL, CL and more exotic M model such as the M-D, Monochrom, et al – it will be interesting to see if they keep the M-A in production, given that Nikon has now exited film camera production leaving Leica as the last man standing.

They’ve also clearly put a lot of effort into bringing consistency to the control and menu layouts across models.

This type of discipline in product development makes sense but, aside from the M and to a lesser extent the Q, it does put them in direct competition with the mainstream of the industry. Currently the SL2 competes directly with the Canon R/R5, Sony A7R III/IV, Nikon Z7/Z7 II and Panasonic S1R. Except for autofocus (which is fine overall but far behind Sony and what I’ve read about the R5), it is competitive and wins in areas like ergonomics (slight edge against Nikon), menu design (best by far) and durability but these come at a substantial premium compared to all except the R5.

It also means Leica will need to iterate at a similar pace to these companies who, especially Sony, do so at a fierce rate. Canon has accelerated their rate and Nikon, while slower, did make meaningful if subtle updates recently as well. There were 4 years between the release of the SL and the SL2 compared with the 2 year (or faster) cycles that Sony, Canon and Nikon run at.

The latest numbers from Japan seem to confirm that Canon is doing well:

https://www.mirrorlessrumors.com/full-frame-mirrorless-market-share-in-japan-canon-gaining-at-sonys-cost/

Also encouraging (for the L-mount) is the (slight) increase in market share for Panasonic.

A really interesting read, thank you for producing this. I was meant to be reading in on new science and stuff for work this week, and this hooked me. It is such a fascinating view from the bridge on the current state of the camera, lens and smartphone industry.

The mere fact that a company like Apple could buy out every single one of our most famous camera brands is staggeringly scary. Yes we know they would not do it, but the fact they could is interesting.

I suspect in four or fives years from now there will be a few less of these companies around. The COVID era will see a few off, and I suspect few of us are out there shooting for fun at the moment. Which will impact on image output too.

Personally I hope a few of our age old favourites find ways to survive, and that we get to a new era of being able to be out and about again.

Keep safe folks, Winter is coming.

Dave

Thanks, Dave. Sorry to have distracted you from your science reading!

Yes, that was part of the intention of including the tech companies and smartphone manufacturers in the company snapshot section: to show the orders of magnitude in difference of scale between them and even conglomerates like Sony and Panasonic. The R&D spending that all of them can put into computational photography alone outstrips what any of the camera manufacturers can, who, in addition, must also investment in lens development and other areas, that smartphone manufacturers don’t necessarily need to.

There is likely to be further consolidation within and exit from the industry.

Personally, am shooting quite a bit – daily photo walks are a respite – but the subject matter is rather limited.

I hope so too.

I see interesting parallels with sales of recorded music; a new digital medium is launched (the CD), sales skyrocket both of the media itself and the equipment with which to play it. This is largely driven by people replacing existing analogue collections with the new ‘improved’ format.

The analogue market collapses, meanwhile the high end digital players are quickly followed by low end mass-market ones of often dubious quality. Sales of these collapse when MP3s become readily available to play and download on smart phones; this market segment was always about cost and convenience not ultimate quality

Various market segments do survive this onslaught — there is a resurgence in high end digital players catering for those invested in physical media; high end network players for those who do not want the compressed sound of an MP3; and, of course, analogue returns in the shape of turntables and both new and secondhand vinyl.

These resurgences are led by a mixture of large companies maintaining a footing and niche companies retaining a steady market share based on the quality of their design solutions and high levels of manufacturing quality.

Sound familiar?

Certainly does, and you are spot on.

That is so true….Well done..

A most interesting and thoroughly researched paper Narain, thanks. As with any expensive purchase, as for example a car, whether the company will keep going and be able to repair a camera is of fundamental importance to me. Otherwise it will soon become a paperweight.

I thought that Mike’s placement of this article alongside that about a younger readership was opportune and some of my comments on that piece are relevant here.

Thanks Kevin, appreciate that – was a labor of love!

It’s a really good point you make and definitely something that I think about when buying a camera and one of the things that will give some people pause about buying one from Ricoh and Olympus and maybe in the not too distant future Panasonic and Nikon.

Took a look at your comments on the younger reader post. A few thoughts:

– While I’m not a deep domain expert, I’d be happy to take a pass at post that covers what artificial intelligence and machine learning do in computational photography on smartphones, which aspects have been ported over to cameras already (mainly in service of AF-C and subject tracking) and which ones haven’t.

– Definitely going to watch those Peter Karbe videos.

– And on the post more generally, agree with the general sentiment about the content on Macfilos – it’s why I (and all of us) are here. But that’s only one part of the equation: driving traffic (from where and how) to the site is the other big one.

Great synopsis, albeit depressing. I’ve pondered the photo future for some time. Daughter is 39, had an Olympus which met an untimely demise in the trunk during an auto accident. My son- 36- will NOT deal with the weight and bags and all the ‘stuff’. Neither will his friends. My daughter thinks about it when she comes to visit and plays with my cameras, but the phone is almost always good enough. Neither they nor their friends EVER think about printing an image. None even remotely care about the mpx count. And the ONE overriding deal breaker is the SD (or equivalent) card. They are NOT going to fiddle around with moving cards to a computer, importing images and maintaining editing apps, no matter how good the final result. My opinion is that step needs to be absolutely seamless, like an iPhone and Photos app. NO cards, ever. Images just need to be there, wherever there is. Leica’s Fotos is way too clunky and slow for their tastes. Zeiss ZX1 may be close.

I think about the twenty somethings and their views. I do know that the SD card approach is DOA. I do think if the camera boys can solve that step, and when all AI enhanced hallucinogenic images look like every other one, there may be a chance for real world camera re-discovery. Case in point, my son has mentioned that instagrams, friends pics, etc are all starting to look like a ‘magazine’- fake, all glowy and saturated. So maybe there’s hope, unless that ‘look’ just becomes the new reality. If the camera manufacturers emulate the computational look of a smartphone, I think it’s game over. I believe they must tread carefully.

I, for one, have no intention of parting with my many pounds of lenses and cameras. They can inherit them- that’ll teach ’em! A last laugh and all that…

There’s nothing like standing in a good rainstorm with a tripod and camera to set the world right!

The lack of a comms function in cameras is the deal killer with the younger digital natives. I have been saying this here for years, but it has largely fallen of deaf ears. Camera companies need to wake up and realise what goes on in 2020. Most images are produced these days for instant consumption and the winners are the companies who are addressing that. Printing images the size of barn doors still goes on, but that is not where the market is heading. I am speaking as someone who wants to get back into film photography, but Covid is preventing me from working in the darkroom that I want to use. However, I do post one image per day on Instagram, which makes me something of an ‘old digital native’.

William

Given that every modern camera has WiFi and that Google Drive and Dropbox – as well as most dedicated photo hosting services – offer APIs (i.e. the ability for third parties to integrate with their services) it somewhat boggles the mind that camera manufacturers (beyond experiments like the Samsung Galaxy Camera, Panasonic CM1 and Zeiss ZX1) haven’t taken the relatively basic and obvious step of adding these integrations, rather than forcing users through the unwieldy process of going via a smartphone app.

I’ve gone back on forth on trying to go all in on smartphone based photography and using dedicated cameras. Per my comment above, I struggle with smartphone ergonomics and a their lack of intentionality.

Bob, take lots and lots of pictures of your kids and family and put them in a box. They don’t appreciate them now but in years to come a collection of memories will be a real treasure, especially when all their digital files are long gone or deleted – the prints will survive and will need no technology to enjoy. It will be the best thing you can leave them.

Put the cameras in the box too..because, well..you never know.

Great insight on the industry, Your crystal ball gives us a great view. I agree w your view Ricoh, but number of street photogs will keep them alive and thought I read where a new unit under development, not sure if it GR. Also like you that nikon z is giving me gas but same w tl2. Any way thank you, really enjoyed.

Thanks, John.

Ricoh have announced a new APS-C DSLR, but no ship date. Details here: http://www.ricoh-imaging.co.jp/english/explore/new_aps-c_dslr/

This was the product I referred to in the post. While there likely is a market for such a camera, it is probably a small one and runs counter to where the industry trends are heading. There is a tiny chance that Ricoh can do for APS-C DSLRs what Leica has done for rangefinders…but it’s a stretch.

There are rumours of a GR IV but, given that there was over 3 years between the GR II and GR III this seems a bit premature and there’s the other question of what they would add. The GR III is pretty feature complete (for what it aims to do) but, equally, somehow a bit soulless compared with the GR II.

Thank you for a thorough and detailed article. I can’t use a smartphone as a photographic tool like many other people I think. Even if the camera industry is slowing down there still will be a market for cameras. However I think that unless you’re a victim of GAS or always want to upgrade to the latest specs, today’s cameras are almost perfect tools (an analog camera is/ was around 22MP). Once people have invested in a system that covers their needs, they’re quite unlikely to invest in another camera or lenses.

Jean

Appreciate that, Jean.

Agree with you regarding smartphones, not for because of their features or image quality, but mostly their ergonomics – there is a lack tactility and engagement that comes from tapping a screen and holding such a thin, slippery device. For me, there’s also a lack of intentionality. When I have a camera with me, it’s explicit use-case is capturing images. Phones do so many different things.

Regarding specs, I think more of it in terms of features for specific use-cases. While not must haves, things like focus bracketing and in-camera focus stacking are (very) nice to have, and legitimately open up different creative opportunities.

Agreed that it’s worth doing the homework to find a system that suits ones needs, but also acknowledge that those needs can evolve over time, both because of one’s growth as a photographer and upgraded technology.

Regarding MP, it was the case that high MP meant trading off against high ISO, but this isn’t really the case anymore with the latest 47 and 61 MP sensors, where the high ISO performance is also excellent. And, the benefit of such high resolution means that, for certain genres of photography, one can swap out a heavy 24-70mm or 24-105mm zoom for a lightweight prime and then crop in post and still have a very workable image.

Ha ha! Thin slippery devices indeed.

I’ve tried taking photos with my iPhone but it feels like trying to make a photograph with a bar of chocolate or a bar of soap! And I’ve lost count of how many times I’ve nearly dropped it, or the touch screen hasn’t responded to my fingers, or it has switched to video or multi-shot mode when I didn’t want it to. That’s before I get to the missing viewfinder which I absolutely need outdoors in sunlight. Just doesn’t do it for me, but I tried, I really did.

Amen to that…

Great article with lots of detail, Narain.

Just some quick comments below.

The peak with digital cameras was never going to last with minor revisions every couple of years etc. The market level is getting more sensible, but there are an unsustainable number of cameras and lens options out there. The market will shake all of that out eventually. Companies like Fuji, Sony and Panasonic and, to a lesser extent, Canon are conglomerates which are not really dependant on the camera market and they could ride out any storm with a reduced model range.. The introduction of digital photography and the ability to merge this with electronic communications has had a very significant effect, particularly in the era of Social Media. Smartphones, or what we might call hand computers with communications and camera functions for the purposes of this discussion, have succeeded because of their ability to deliver that combination in a compact package. Digital cameras today are essentially imaging making computers with lenses attached. The thing that I find most surprising is that most cameras are still based on the mid 20th Century concept of a 35mm SLR or the same with an electronic screen in place of a mirror and prism. Listening to Peter Karbe of Leica speaking last week it is obvious that we have not yet even remotely seen the capabilities of computational photography except perhaps in Smartphones, but things like lens profiles in camera or in Lightroom are the first baby steps along that route. The Leica M is a bit of anachronism, but long may that continue, notwithstanding the price of such craftsmanship.

My summary of the digital camera market would be ‘ a lot done, a lot more to do and still all to play for’.

I haven’t mentioned Covid and the ‘new normal’ as none of us can predict where that is leading.

William

Thanks, William – appreciate the detailed reply.

Agree with you that camera manufacturers have to step up their investments into computational photography in order to remain competitive – and, yes, we’re only just seeing a sliver of the dividends that this will yield.

On your point around consolidation of camera models, I think this is a bit more nuanced and, in fact, more tied to your point around camera design. Manufacturers have segmented, and continue to segment, the market (and consequently their product lines), in ways that are increasingly outdated and arbitrary: this model for video, this for stills, best autofocus and high FPS in this sports model, max MP in this model, etc. To your point, one thing that smartphones have shown us is that, by being computers first (and cameras, or GPS devices, or phones, or whatever else second) is the flexibility that approach offers.

Put in crude terms, the iPhone has offered 4K/60FPS since the iPhone X, which launched in 2018, while there are still reasonably high-end cameras launching today that don’t offer this. While not a feature that everyone needs or wants, the point is that for those who do, it’s there (even if the iPhone isn’t a specialised video capture device).

The same goes for what Apple calls Deep Fusion (not dissimilar to XD Fusion graphic above, in the Huawei section) where multiple bracketed exposures are analysed for quality, dissembled to extract the highest quality elements and then reassembled into a single high-quality image – when will something like this come to cameras and who will do it?

In terms of the companies in play, despite their being a conglomerate and because of the image sensor business, it looks like Sony is in it for the long haul. Canon, too. Fuji has seemed in a good place to date, but, yes, it’s a crowded space. Panasonic seems to be the most indifferent to the camera business.

Great article and the detail is exceptional. I’ve never thought much about the greater picture behind the products on the shelf of my local camera shop, but this article gives a fascinating perspective. Thank you for all the work and effort that must have gone into this. Macfilos just gets better and better.

Appreciate the feedback and kind words, Roger. There’s a long road between research and development and cameras ending up on the shelves! Competition from smartphones, and their annual upgrade cycles, is certainly putting pressure on camera manufactures to speed up their development cycles. Canon seems to have responded well here, investing first into lenses (which have a longer life cycle than bodies) for the RF mount and then moving quickly to evolve from the R and RP to the R5 and R6.

For digital, Leica SL2 and Q2 are already as perfect as I really need so I’m not wanting more perfect photographic devices. I would like more film cameras and Kodachrome 64 back!And while I’m at it,I’d also like Minolta and Contax back. Maybe i just need a time machine.

Thanks for the comment, Steven. I’m an SL2 user as well and am mostly very happy, though the Nikon Z series is a regular temptation (the Z6 replaced my old SL, which was replaced by the SL2 and there’s a non-zero probability that the Z7 II might replace the SL2…)

For film, the first camera I loved was a Contax S2, so I empathise!

Narain, thanks for your comment too! I still happen to have a Contax T2 and an Aria which get occasional use since I’m lucky to live in an area of Japan where i can still get easy access to film processing. In fact I used to live just around the corner from the factory in Okaya where the cameras ( or parts for them) were made ( About 25 years ago now which is scary to think about!) I well remember in those days, the railway station always had a glass display case proudly showing off the local products and i would often peer in at the Contax S2 and 137 on display there (along with other mysterious bits of machinery from other companies in the area like Seiko Epson). on my way to work every morning.Those Contax models always had lovely ergonomics and design without being cluttered with controls.To my mind, The current Leicas have a similar build which is why i like them so much.

I’ll add to your comments about technology and the direction of the market by saying that some of the best cameras produced in Japan came to be put in production, because in many cases the heads of those companies happened to be keen photographers themselves and had a personal interest in the cameras and were in a position to support the projects.Where that is not the case, decisions were made solely on trends, marketing and profits. Ricoh, for example, doesn’t actually need to make cameras, Most of their money comes from their printer business ( and believe me, they are in almost every office in Japan!), Olympus makes most of it’s money from their medical products division. Yet somebody, somewhere in these companies is passionate enough about photography that both companies make some wonderful cameras like the GR series and the OM-D series. Let’s hope future CEO’s for the big camera companies remain passionate about cameras!

As we all well know, we have the Leica today because of that one historic “Let’s make it” decision, We have Apple computers because of Steve Jobs’ determination to make them.

By the way, well done for listing the sources for the article! Appreciated.

Nice!

London (where I’m presently) also a good city for film photography, as I’ve discovered with a recently acquired Nikon FM3a. It’s a camera that in many ways reminds me of the Contax S2 – agreed with you about the superb ergonomics.

That’s a very valid point about executives at Japanese camera companies and, as one can see in this video – https://www.youtube.com/watch?v=Qe3AteY8NuQ&t=1116s – that certainly seems to be the case at Pentax.

While slim on information, one gets the same feeling from Nikon executives in this interview: https://www.dpreview.com/interviews/3679521489/nikon-interview-its-time-to-get-excited